Are There Fences in the Global Factor Zoo?

Regional and global factor momentum signals outperform local factors in forecasting risk premiums and revitalize momentum investing in less-integrated markets like Japan.

2024-04-01

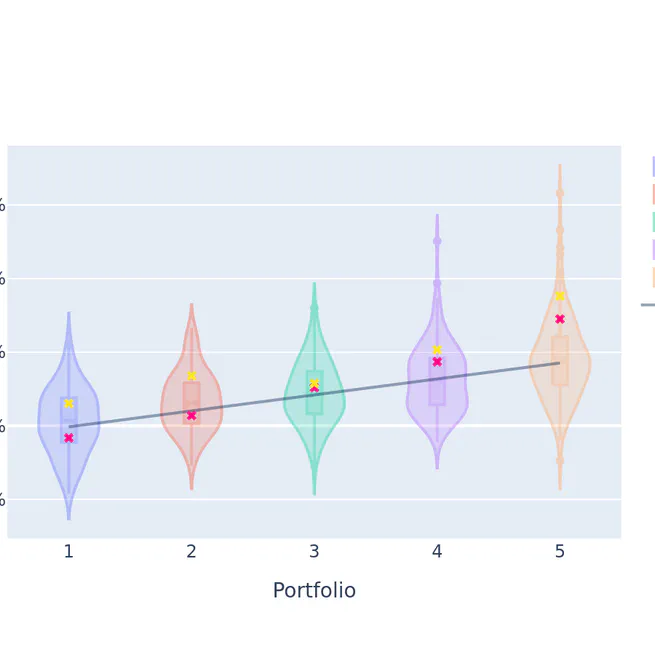

Lost in Translation: How Predictability Turns into Performance

This paper proposes ranking-based portfolio optimization to mitigate the effects of parameter uncertainty, improving Sharpe ratios and reducing portfolio concentration.

2024-01-01

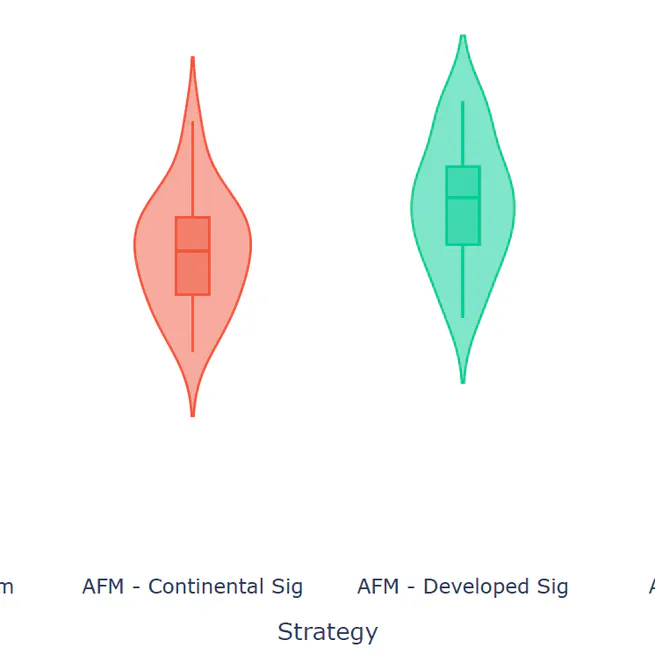

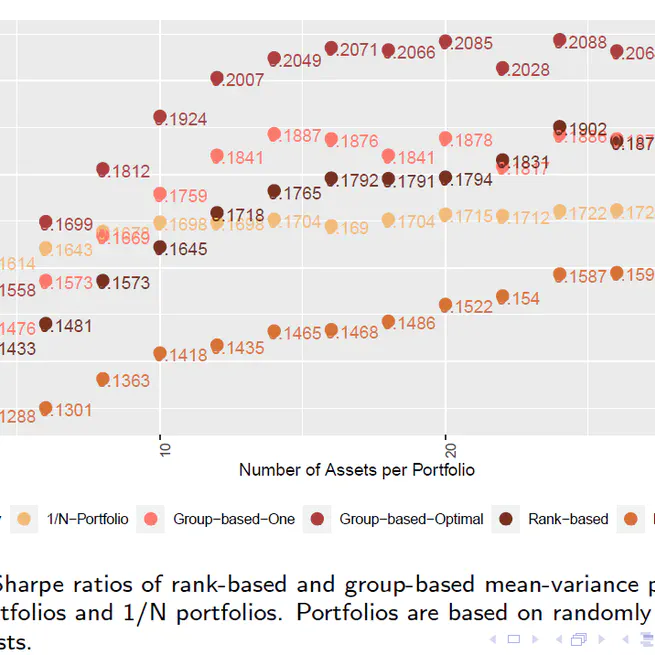

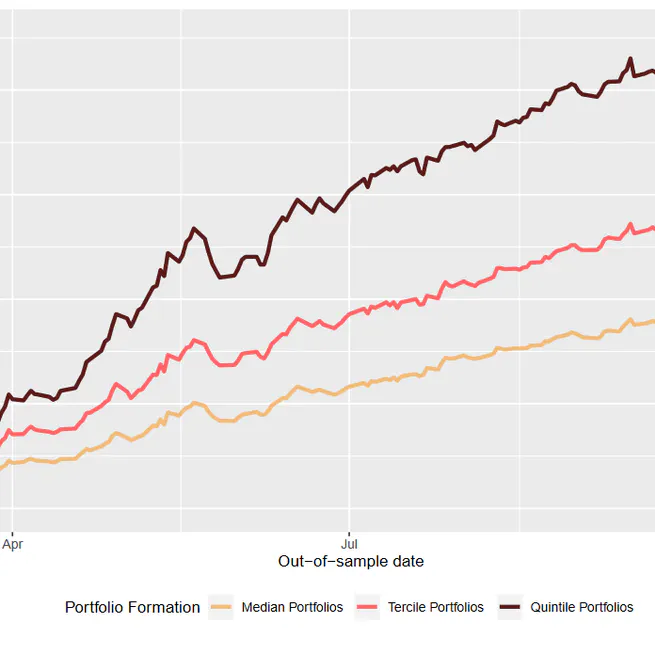

Less Is More: Ranking Information, Estimation Errors and Optimal Portfolios

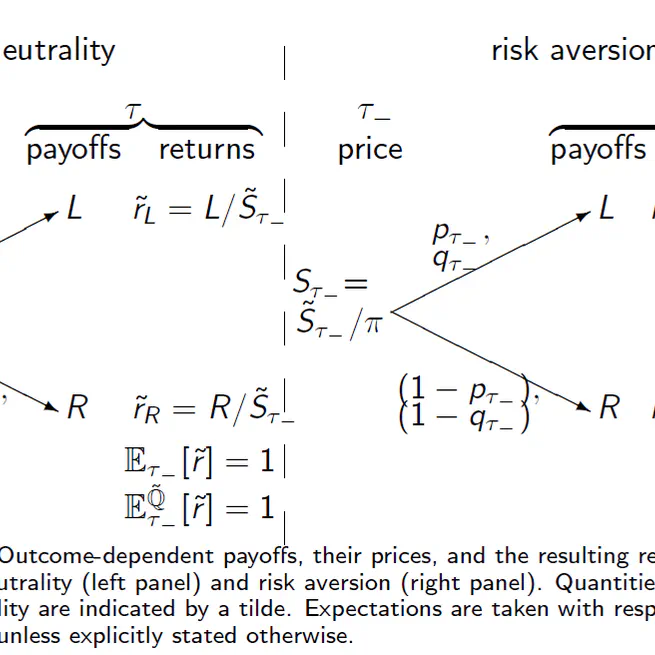

We offer a novel approach that aims at mitigating the crippling effects that parameter uncertainty and estimation errors have on the out-of-sample perforance of mean-variance optimized portfolios. We argue that investors should not rely on exact forecasts when optimizing portfolios but instead base their optimizations on ranking or grouping information and thereby implicitly reduce the informational content of their parameter inputs.

2024-01-01

Factor Chasing and the Cross-Country Factor Momentum Anomaly

We document a cross-country factor momentum anomaly, which we term 'Factor Chasing'. Specialized style mutual funds chase factor returns across countries, but their trades are delayed, leading to positive returns that are not spanned by leading factor models.

2024-01-01

Event Risk Premia and Non-Convex Volatility Smiles

We analyze event risk premia in an expected utility framework and provide closed-form solutions under both quadratic and power utility for four different cases: Deterministic/stochastic conditional event returns, and deterministic/stochastic event outcome probabilities.

2024-01-01

Estimating Crypto-Related Risk: Market-Based Evidence from FTX's Failure and Its Contagion on U.S. Banks

We estimate crypto-related risk for U.S. banks using historical covariance with bitcoin returns, focusing on contagion from FTX's failure.

2023-09-01

Parameter Uncertainty, Financial Turbulence and Aggregate Stock Returns

In this paper, we develop a novel, intuitive and objective measure of time-varying parameter uncertainty (PU) based on a simple statistical test.

2020-02-05

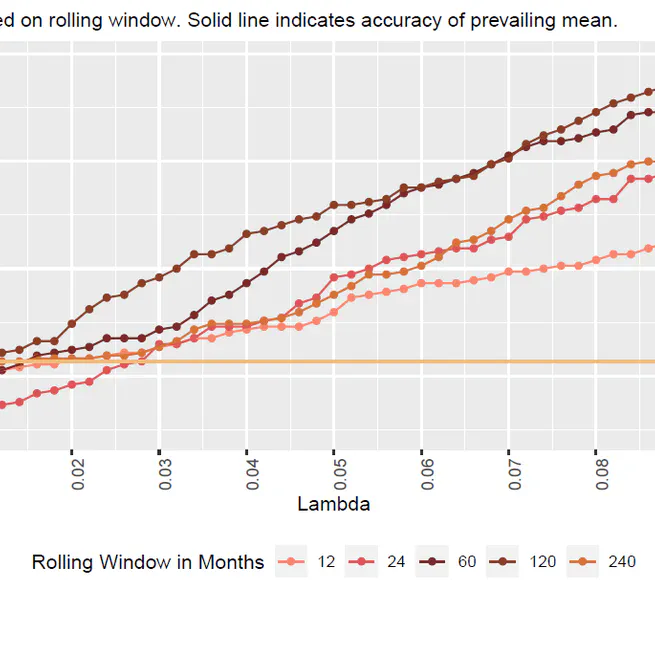

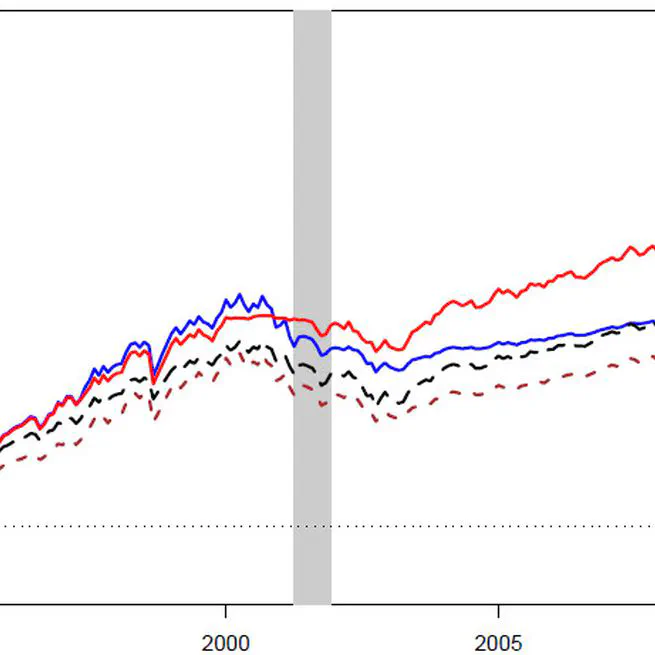

Turbulence in the Cross-Section: Predicting Factor Premia

We show that parameter uncertainty based on the turbulence within each cross-section of factor portfolios produces a significant out-of-sample forecast for six out of seven tested Fama-French risk factors.

2018-07-28

Towards a Well-Founded Valuation of Managerial Flexibilities in IT Investment Projects - A Multidisciplinary Literature Review

Based on a multidisciplinary literature review, we discuss the assumptions implicit in the prevalent Black-Scholes model and argue for relaxed assumptions that better represent characteristics of uncertain IT projects.

2016-10-12