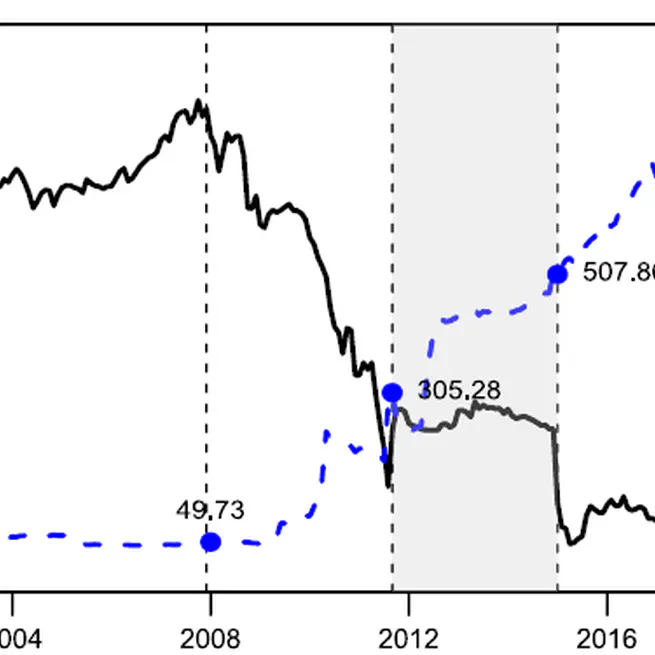

Regime-Dependent Drivers of the EUR/CHF Exchange Rate

We analyze drivers of the EUR/CHF exchange rate in different regimes between 2000 and 2020, estimating structural breaks in an integrated way together with the drivers that are relevant during these subperiods.

2023-02-14

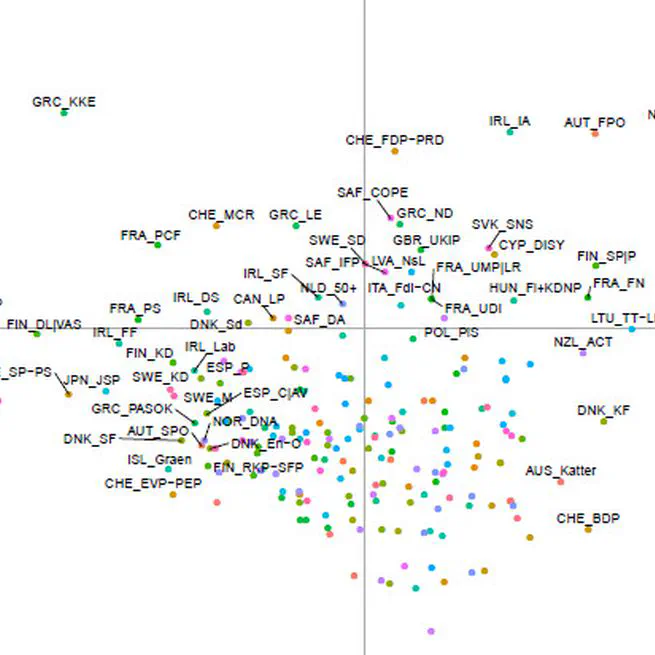

The Price of Populism - Financial Market Outcomes of Populist Electoral Success

We examine the effect of populism on financial markets around national elections. We find that the electoral success of populist parties has a direct impact on volatility in major domestic market indexes with different signs depending on the political ideology of the populist parties.

2021-09-01

Higher Moments Matter! Cross-Sectional (Higher) Moments and the Predictability of Stock Returns

In this paper we investigate the predictive power of cross-sectional volatility, skewness and kurtosis for future stock returns.

2020-09-07

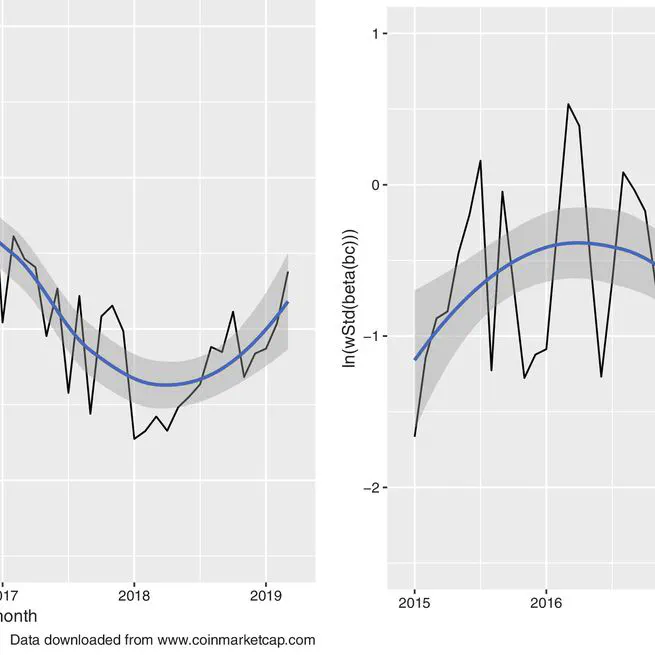

Cryptocurrencies: Herding and the transfer currency

This paper investigates herding behavior in the crypto market. We consider the full, survivorship-bias free cross-section of cryptocurrencies, and document - against existing evidence - significant herding in this dataset. The effect is stronger, when using bitcoin as a *transfer currency*.

2020-03-01

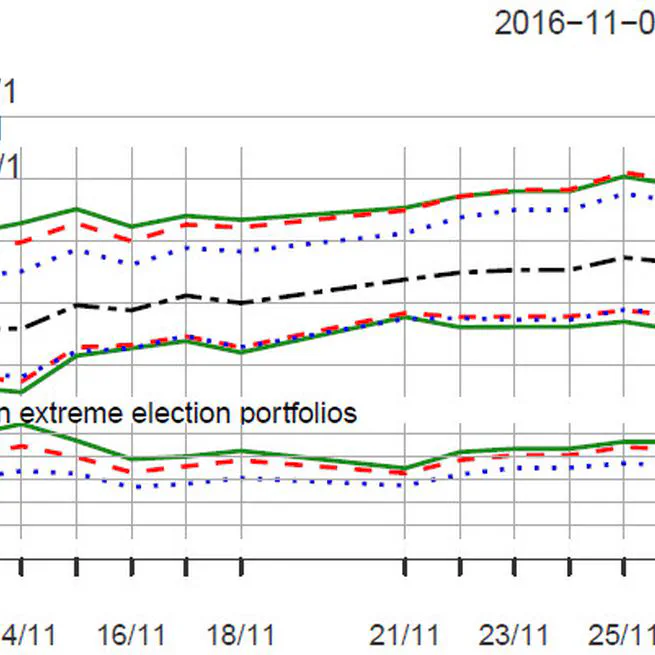

Political Event Portfolios

We use data from betting markets to analyze the sensitivity of stock returns to potential outcomes of political events such as elections. By classifying stocks into expected conditional winners and losers prior to such an event, we form portfolios that generate large positive returns after the event date, conditional on correctly anticipating the outcome. We illustrate this using data from the 2016 US presidential election and the 2016 Brexit referendum.

2020-02-25

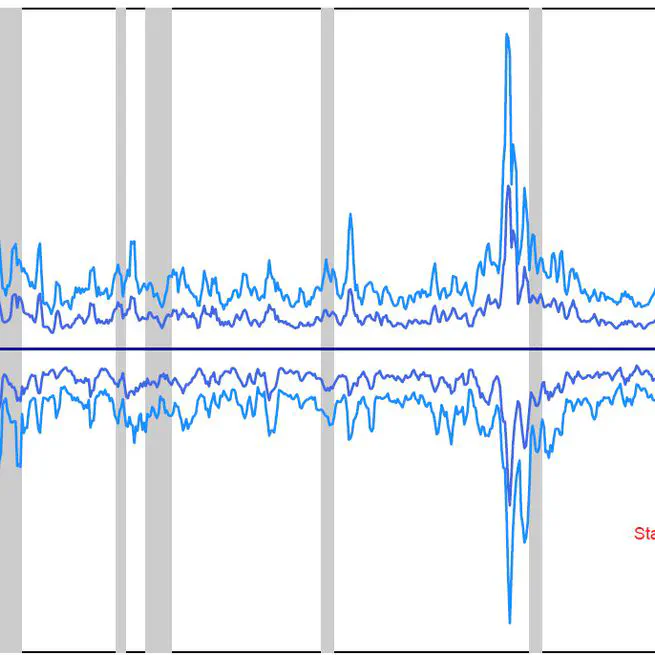

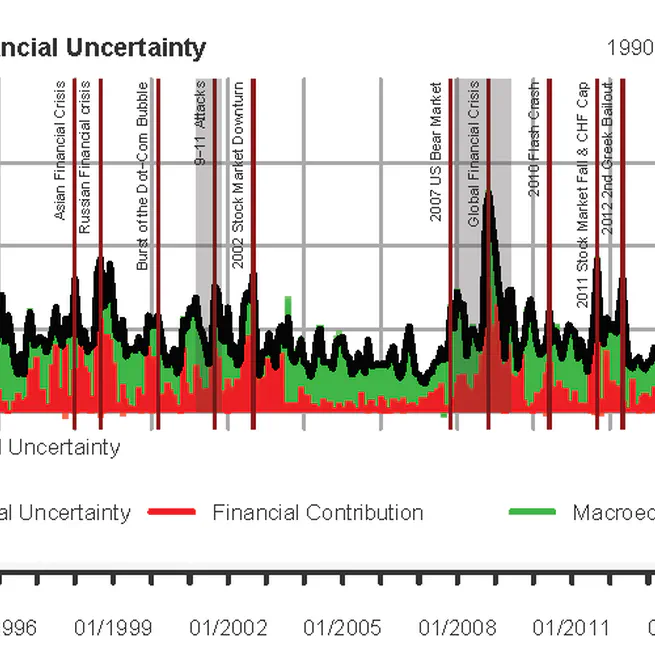

Credit Intermediation and the Transmission of Macro-Financial Uncertainty: International Evidence

This paper introduces a novel measure of global macro-financial uncertainty and examines the state-dependent transmission of uncertainty to economic activity.

2020-01-21

What Drives Our Beer Consumption? - In Search of Nutrition Habits and Demographic Patterns

In an unbalanced cross-country panel covering 169 nations and time-series records of up to 52 years we analyze drivers behind beer consumption.

2019-09-02

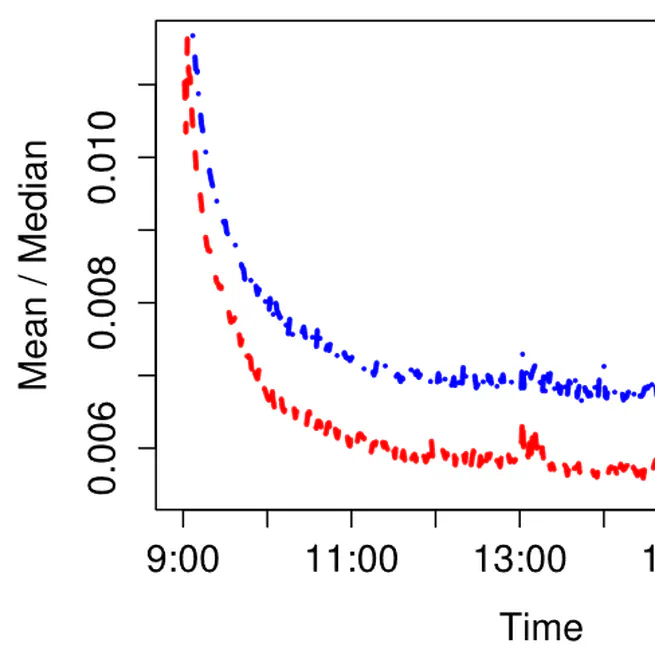

Bid-Ask Spread Patterns and the Optimal Timing for Discretionary Liquidity Traders on Xetra

This paper explores the statistical and economical significance of intraday and -week patterns in bid-ask spreads.

2018-07-01

PRIX – A risk index for global private investors

The purpose of this paper is to create a universal (asset-class-independent) portfolio risk index for a global private investor.

2017-02-03

Decision Support for IT Investment Projects

Based on a thorough review of the literature, this paper discusses the assumptions of the Black-Scholes model and presents an advanced simulation model for the valuation of real options in IT investment projects.

2016-03-08